Product AB are produced in large batches while Product CD are as specialty line that only a few customers buy. The IASC and IOSCO.

Accounting Principles Explanation Accountingcoach

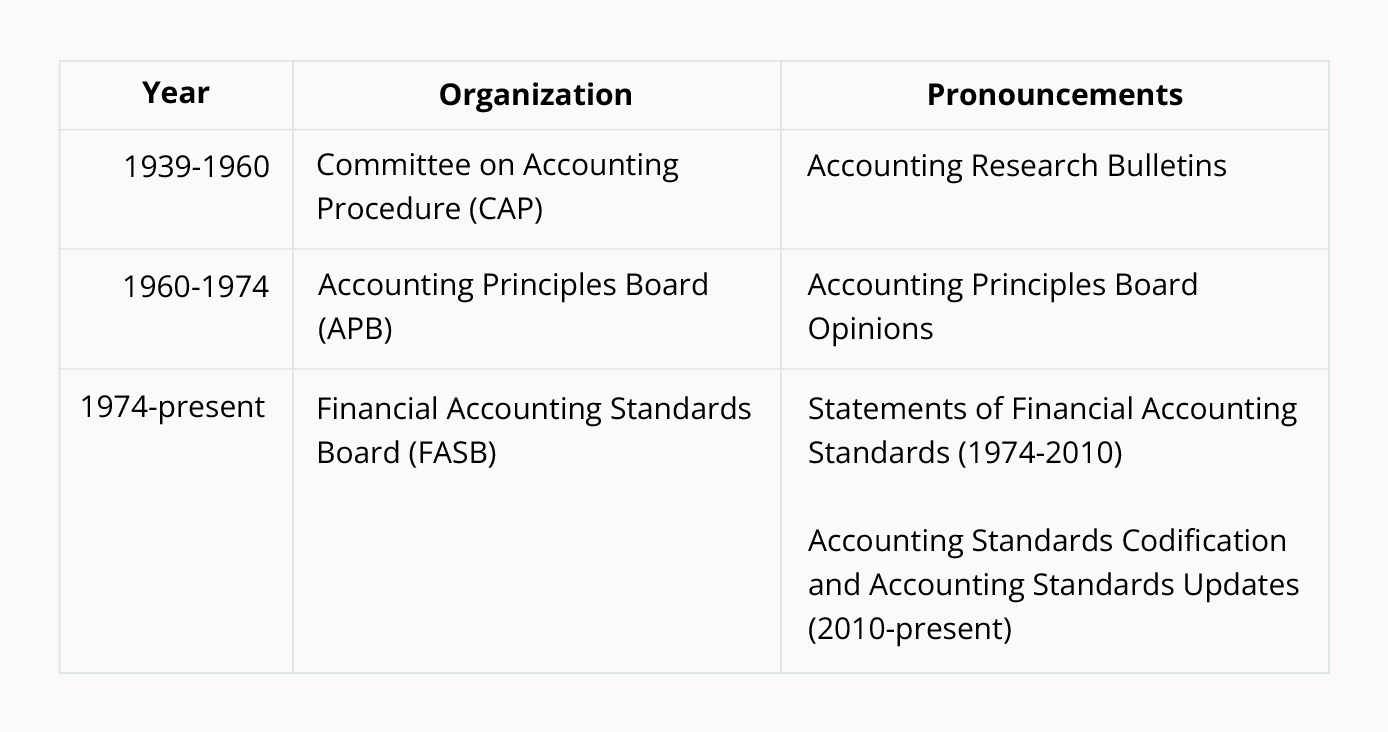

Over the years accounting standards have been developed by different accounting authorities.

. To agree on the scope of accounting and of principles or standards is admittedly. The FASB is the private sector group presently charged with that. A change in accounting standard can have a huge redistribution of wealth in the economy.

Accounting standards apply to the full breadth. Evaluate this process citing an example. The second is that changing accounting standards will have consequential effects of some sort.

See doc 10 CPAs are licensed by. Let us see the main objectives of forming these standards. The standard-setting body must consider potential economic consequences of a.

The International Accounting Standards Board. Can overrule the FASB when their policies disagree. 132Accounting standard-setting has been characterized as a political process.

2 The process of setting accounting standards has been characterized as a political process. The setting of accounting and reporting standards often has been characterized as a political process. The International Accounting Standards Committee IASC is a private sector body whose membership includes all the professional accountancy bodies that are members of the International Federation of Accountants IFAC.

Evaluate this process citing an example. 133What are the key provisions of the Public Company Accounting Reform and Investor Protection Sarbanes-Oxley Act of 2002. The process of setting accounting standards has been often considered as a political process.

Promotes the use of high-quality understandable global accounting standards. The following points highlight the four major difficulties faced in setting up accounting standard. Accounting standard setting has been characterized as.

Using the scientific method. Was the predecessor to the IASC. Now because the financial statements have to be made following the standards the users can rely on them.

The company is concerned that using DLH is inappropriate because some costs are driven by other activities. Accounting standard-setting has been characterized as. Conflict in Accounting Theories 4.

These accounting standards have been prepared to meet the needs of the international financial industry for standardised accounting reporting that can be relied on for uniform presentation of information. IFAC has more than 140 members from over 100 countries. An accounting standard is a set of practices and policies used to systematize bookkeeping and other accounting functions across firms and over time.

The most political issue in the FASBs most recent deliberations and pronouncements. The process of setting accounting standards has been characterized as a political process. Promotes the use of high-quality understandable global accounting.

Using the example of marking assets and liabilities. Some common examples of accounting standards are segment reporting goodwill accounting an allowable method for depreciation business combination lease classification a measure of outstanding share and revenue recognition. Accounting standard setting has been characterized as.

Securities and Exchange Commission SEC The. Zieky et al 2008. 3 Pension plan accounting.

9 What are the main provisions of the Public Company Accounting Reform and Investor Protection Act of 2002 Sarbanes-Oxley. In this section we emphasize the relationship of the standard setting process to test development. Setting Standards.

The GAAP accounting standards have been largely developed within the United States while the IFRS accounting standards are more European based. 134With respect to the financial statements what is the value of an audit. The most recent example of the political process at work in standard-setting is the heated debate that occurred on the issue of.

Using the scientific method. Accounting standard-setting has been characterized as. They know that not conforming to these standards can have serious consequences for the companies.

The first is that standards of financial accounting and reporting are needed as is. Evaluate this process citing an example. An accounting standard is relevant to a companys financial reporting.

As mentioned earlier the standard setting process has been well documented in several sources Cizek. 2 The process of setting accounting standards has been characterized as a political process. Was the predecessor to the IASC.

Using the scientific method. Accounting for business combinations. Difficulties in Definition 2.

Accounting questions and answers. The International Accounting Standards Board. Can overrule the FASB when their policies disagree.

Discuss this proposition giving an example. Changes in standard can have significant impact on companies investors and creditors. Accounting for postretirement benefits other than pensions.

Has its headquarters in Geneva. The Financial Accounting Standards Board FASB in the United States and the International Accounting Standards Board IASB in the United Kingdom. In a standard setting process the FASB encourages the board participation to take and consider the shareholders and public advice thus it is considered as a political process.

Over time accounting standards have developed to reflect changes in the business world as well as changes in our ability to account for such changes. 8 Accounting standard-setting has been characterized as. Was the predecessor to the IASC.

The company works about 100000 DLH per month. Political Bargaining in Standard Setting 3. Some mechanism for setting these standards.

Of standard-setting at the US. Hambleton. While setting standards appropriately is critical to.

Using the scientific method. The following information regarding cost pools and drivers has been developed. The process of setting accounting standards has been characterized as a political process.

Hence the process of setting accounting standards is a complex task. Two of the most respected standard-setting bodies are. The main aim is to improve the reliability of financial statements.

We make suggestions for how research on the politics of standard-setting can progress in the future. Financial Accounting Standards Board FASB1 Although some important questions have been answered our current understanding of the politics of standard-setting is relatively modest and more remains to be done.

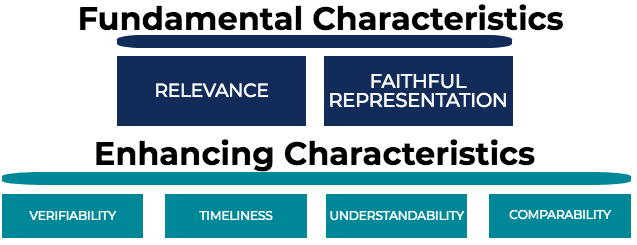

Qualitative Characteristics Of Accounting Information Overview Guide

Overview Of The Structure Of The Ifrs Foundation And Iasb

Accounting Standard Overview History Examples

/paper-with-title-international-financial-reporting-standards--ifrs---850740234-6e303822ed5e4800b523b0ac24db396c.jpg)

International Accounting Standards Ias

0 Comments